How government twisted the health insurance industry into a bloated, inefficient de facto government program.

by Rob Roper

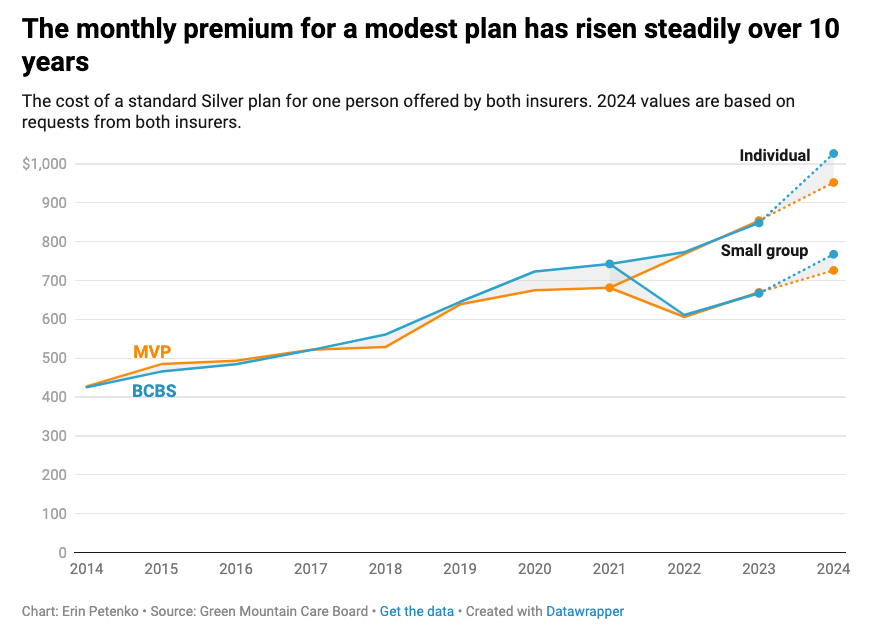

In what has become an annual story with the predictability of the seasons, Vermonters are about to get whacked with a huge increase in their health insurance premiums. Blue Cross Blue Shield is asking the Green Mountain Care Board for an 18.1 percent increase for plans sold to individuals and families on the state-run marketplace and a 17.6 percent increase for plans for small groups, businesses, and municipalities. MVP is asking for increases of 13.8 and 14.3 percent respectively. All this would be on top of the 11.4 percent increase Blue Cross got last year, and the 19.3 percent MVP got.

Since 2014 and the passage of the so-called “Affordable Care Act,” (I know, LOL!) healthcare premiums have nearly doubled in cost. Don’t blame the insurance companies, blame the politicians.

Insurance is supposed to be a risk management tool. It’s not supposed to be some sort of pre-paid, discount, subsidized healthcare. Here’s how insurance is supposed to work:

Say there are ten of us, and the odds are that one of us in the next ten years will get Widget’s Disease, which will cost $100 to treat. So, the ten of us, with the help of an insurance company, agree to each pay $1 a year in premiums for ten years (plus a small commission to the insurance company for doing the work of brokering this deal), the total of which comes to the $100 needed to treat one case of Widget’s Disease. The unlucky one of us who gets the disease gets the $100 to pay for his or her care.

This works because everyone is sharing equal risk and benefiting from the plan by minimizing and stabilizing the potential cost of a future health event. Each member of the pool is buying the financial security that comes with having a predictable, manageable $1 a year premium for ten years rather than having to cope with a potentially unmanageable $100 expense at some unknown point in the future.

Now, some folks might decide they’d be better off pocketing the $10 over the ten years and hope they’re in the 90 percent that doesn’t end up getting Widget’s Disease. If you’re right, yeah, you’re better off financially for sure. But if you’re wrong, you’re screwed. That’s the risk you choose to take.

Some people will make that bet, hope they don’t get sick – but they do.

Some don’t have the dollar a month to begin with and can’t participate even if they want to. There are others who are born with a congenital version of Widget’s Disease, and thus the odds of them needing treatment are not maybe ten percent in the future, but rather 100 percent right now. A fair premium based on risk assessment for such patients when they need care would be, therefore, 100 percent of the cost of treatment — plus commission. I hope it’s obvious that paying for healthcare this way makes no practical sense.

The solution for folks in these situations is not – cannot be — insurance but must be by definition a form of charity, either private or through some sort of government program. This should be kept separate from the business of selling insurance to manage future financial risk.

But count on government to predictably FUBAR the situation.

What government does now is mandate that the insurance company issue a policy to people with pre-existing conditions (“guaranteed issue”) at the same price that the folks who have been assuming the costs of managing that one-in-ten risk factor (“community rating”). This is no longer insurance; it is government mandated, subsidized care that forces private insurance businesses to take on the role of a government welfare program – and their customers the role of taxpayers.

It is both incredibly unfair and stupendously inefficient. (It is also Mussolini’s definition of fascism: “The marriage of corporation and state,” so there’s that fun little aspect to this as well….)

Continuing with our Widget’s Disease example, the folks who are buying insurance to manage their financial risk are paying a dollar a month for ten years to cover the cost of the one treatment regimen the group will end up needing. But the government then says, hey, this other guy here didn’t want to pay the premiums before, but now he has Widget’s Disease, so you all need to let him into your group at a dollar a month.

This person will immediately draw down the $100 treatment payout, which means that in order for the original ten members of the pool to still have a payout when one of them gets sick, they will have to pay $2 a month in premiums instead of $1. This is a de facto tax on the original members of the risk pool to cover the cost of charity medical care for someone who assumed no risk and bears no or very limited costs. Not fair, and not transparent policy.

Government makes things even worse with mandates. Say, you’re one of the folks at risk for Widget’s Disease, but not for Doodad’s Syndrome. You’re willing to pay for a policy that covers the former, but not the latter. No, no, says government. Not allowed. It won’t let the insurance company write such a policy. If you want coverage for the thing you’re actually at risk for, the politicians force you to pay, say, another dollar a month on top of that to cover the thing that you’re not at risk for at all. (Real world example: making the nuns pay for pre-natal coverage). So, instead of $1 a month, now you’re paying $3. This is, again, a de facto tax added to the cost of your premium to subsidize someone else’s risk.

So, if you’re scratching your head as to why you can’t afford health insurance anymore after our legislators passed a bunch of laws and installed an entire board of experts promising to make it more affordable, well, this is a wildly simplified explanation of why.

Politicians have twisted insurance away from covering the much lower cost of shared future risk into a mechanism for paying for everyone’s immediate healthcare needs right now. And immediate healthcare costs 100 percent of what healthcare costs. Which begs the question, if health insurance premiums cost as much or more than what your future healthcare needs are likely to be, what good is insurance at all? A question many of us are probably asking at the moment.

All that said, of course, we don’t want to just leave sick people who can’t afford insurance or health care out in the cold. But what these people need is immediate access to doctors, nurses and hospitals, not a financial instrument designed to limit the potential impact of a future expense. Giving them the latter when they need the former is A) stupid, B) not particularly effective or compassionate, and C) financially inefficient.

If we would simply leave the private health insurance businesses alone to create policies that consumers want to buy covering risk factors that applicable to those customers, the overall cost of health insurance would fall dramatically. Many more people would be able to afford insurance – in the legitimate definition of what insurance is: as financial instrument designed to limit the risk of a future healthcare related cost.

For those who remain uninsured or uninsurable because they have a preexisting condition and need access to healthcare now, it will require some form of private charity and/or government program that helps them to gain access to that care. This isn’t a radical concept. For example, if you lost property during the recent flooding, you cannot get retroactive “guaranteed issue” flood insurance for your home’s pre-existing condition, but there is help for you in the form of FEMA and other government programs (not to mention a whole bunch of neighbors with buckets, shovels, and fans).

This is how healthcare and health insurance should work. What the cost of a safety net would be will have to come about through open, transparent, political debate, so those who make these decisions can be held accountable – which, of course, is why politicians don’t do it this way. There is no amount of money they won’t waste if it will ensure you blame someone else – in this case insurance companies – for the harm they’re causing you.

Rob Roper is a freelance writer who has been involved with Vermont politics and policy for over 20 years. This article reprinted with permission from Behind the Lines: Rob Roper on Vermont Politics, robertroper.substack.com

Discover more from Vermont Daily Chronicle

Subscribe to get the latest posts sent to your email.

Categories: Commentary, Health Care

This is an excellent summary of the problem. The fact that even at the national level Republicans have not been able to counter these developments with the kind of logical explanation Mr Roper offers shows that the entire DC crowd is in on it. They want to have more centralized control over our lives. We need the kind of revolution that #Vivek2024 is talking about.

The mandates are creating a cost problem as well as political and social divisions,

as when gov’t steps in and forces insurers to cover contraception and gender “reassignments”. Let’s be honest, birth control is not really a medical issue for most people, it is an entertainment expense sometimes incurred when intimately associating with another human. Health insurance doesn’t cover flowers, motel rooms, eyeliner and high heels. If you enjoy swimming, health insurance shouldn’t pay for your swim suit or goggles. If gardening is your thing, it doesn’t cover work gloves or wide-brimmed hats. To have a practical and sustainable system that covers MEDICALLY NECESSARY practices and procedures, there have to be coverage limits based on science, not feel-good leftist philosophy.

An apt but long winded oration, Rob- to accurately convey the message that- Yet again, the Vermont legislature has intentionally made a mess for the Vermont citizen.

Health Care, Education, Day Care, Energy, Transportation… need we continue?

More to the point, for Vermont voters to continue as in the past, we will collectively become a ruined state. Due to the election changes forced thru in 2020 by the legislature, we may be too late.

Bigger government means less freedom and choice but always more taxes to support it. Vote them out of office and TAKE BACK VERMONT!

Maybe I’ll establish residency in Arizona.

It’s obvious that nobody here, including the author, has suffered a catastrophic illness, has a parent, partner or child who has suffered a catastrophic illness or requires an outrageously expensive med in order to live and breathe. Smug, know-it-alls.

We’re all still waiting for The Orange One’s promise of “The best healthcare. The most tremendous healthcare. Fantastic. Terrific. A big, beautiful plan the likes of which the world has never seen before.”

Try Self-pay for an MRI or two up at UVM and choke paying for them.